Crude Awakening

Market expectations shifted notably this week as interest rates fell and the link between bonds and oil prices—prevalent since the start of the Iran War—broke down. Since the start of the conflict, surging crude had kept traders on alert for renewed inflationary pressure and a more hawkish Federal Reserve. However, by the end of the week, Treasury yields were moving lower even as oil stayed elevated, signaling a change in how investors interpret data and headlines.

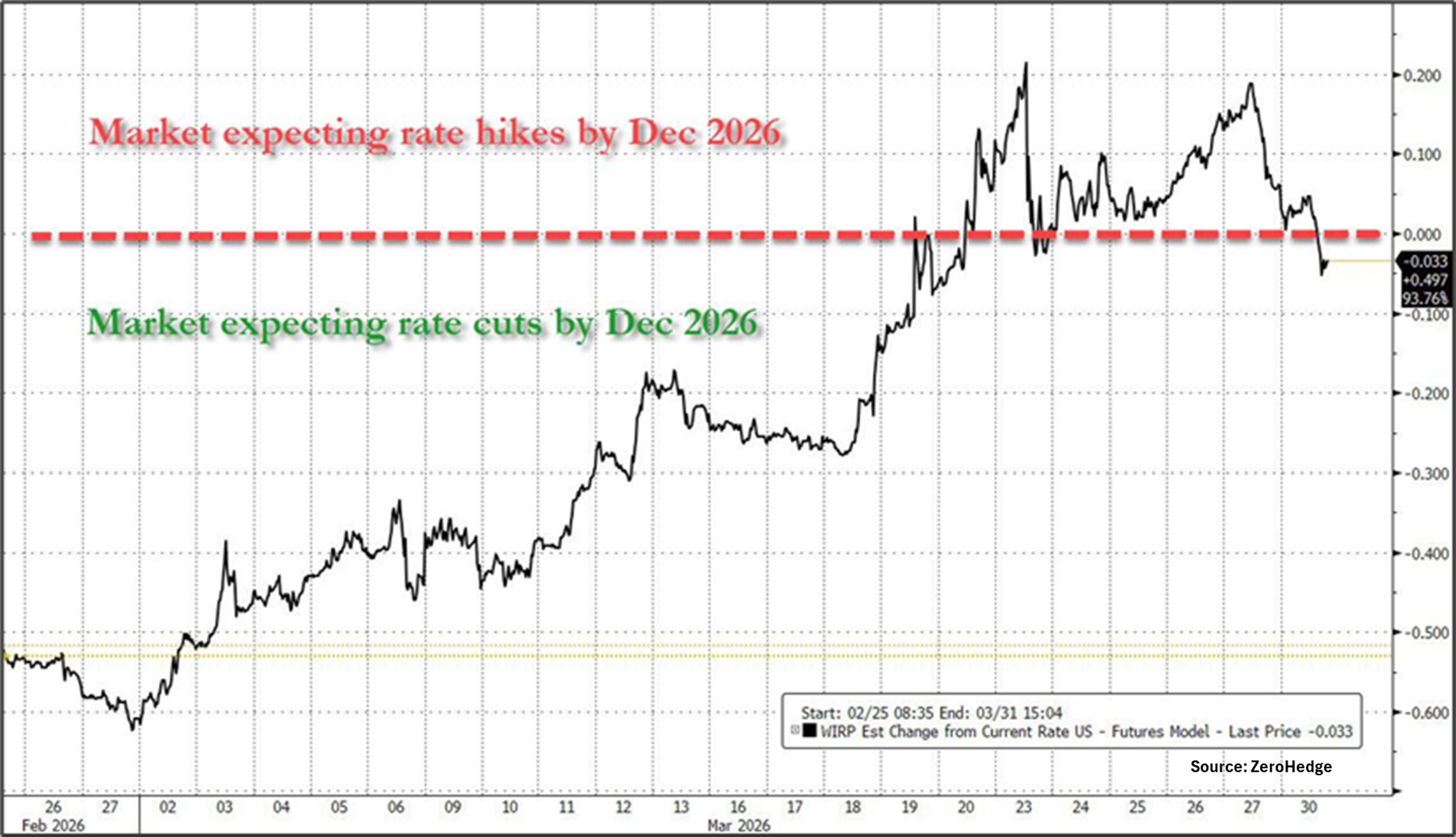

The chart below shows how rate expectations have changed since the start of the war, moving from a hawkish tone (i.e., fewer rate cuts) toward projected rate hikes. That narrative flipped this week as rate expectations reversed course, shifting focus toward a slowing economy rather than inflation. This trend has been solidified by several large banks, including Goldman Sachs, which are forecasting an increasing risk of a recession over the next 12 months. While a recession is not the base case, the change in direction is noteworthy.

Markets are starting to move away from a simple inflation narrative toward a more cautious view of growth. Even as oil and other input costs remain a concern, investors appear increasingly focused on whether those price pressures will slow consumer spending and reduce hiring enough to weaken the economy. That shift matters because it changes how traders interpret higher energy prices: instead of assuming they will force the central bank to stay hawkish, many are now wondering whether the primary effect will be a drag on demand that eventually cools inflation on its own. That scenario would invite Fed intervention to lower rates and push the economy toward stronger growth.

For investors, this break in correlation is important because it shows the market is no longer following one simple macro narrative. Instead, it is balancing two competing stories: the rise in oil prices due to the Iran War is a warning about inflation, while falling rates are a warning about growth as high oil prices create demand destruction. This split is likely to keep volatility elevated.

What central bankers fear most is a rise in inflation expectations coupled with a weaker growth forecast. In that case, they must decide which problem to address first. If they prioritize inflation, they would raise interest rates in the face of a weakening economy. Pushing a fragile economy over the edge would solve the inflation problem quickly, but the recovery would be longer and harder. If they address weaker growth first, they would reduce interest rates to stimulate the economy; however, this would also “feed the inflation beast.” A prolonged move higher in oil prices will place the economy on that pathway. The only way to avoid this is a de-escalation of the war soon, as it can take a very long time to recover from a physical supply shock.

Which way this is headed seems to change by the hour. Don’t get caught up in the headlines, and remain a believer in the fundamental resilience of the U.S. economy.

Have a great week!

What We’re Reading

-

Microsoft closes worst quarter on Wall Street since 2008 on AI concerns: ‘Redmond is in a pickle’

-

SpaceX confidentially files for IPO

-

Meta, Google under attack as court cases bypass 30-year-old legal shield

-

U.S. payrolls rose by 178,000 in March, more than expected; unemployment at 4.3%

Palumbo Wealth Management (PWM) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where PWM and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at www.palumbowm.com.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be dependable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

All information has been obtained from sources believed to be dependable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that no such statements are guarantees of any future performance, and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

Past performance is no guarantee of future returns.

Crude Oil, Fed, Federal Reserve, Interest Rates, Iran War, Lowering Interest Rates, oil crisis, Raising Interest RatesBy: Adam