Houston, Do We Have a Problem?

- On Apollo 13, the problem was quickly recognized. In today’s economy, there are still plenty of questions. We hate to be part of the gloom crew, but when you step back and look at the world through a wide-angle lens, it’s is increasingly hard to be optimistic. The world is experiencing the first major energy crisis in a very long time, and it appears to be of our own making.

- In our rush to help the needy during the pandemic, we unleashed massive liquidity unlike anything ever seen before. The result appears to be too much money spiking demand for goods and services at a time when supply is limited due to the pandemic. The result? Shortages and price inflation.

- In our rush to ‘be green’ we have apparently flung ourselves quickly into a future that is fraught with complexity. Mandating renewables over fossil fuels, and EVs over internal combustion vehicles, will not solve our carbon problem, as we appear to be discovering now. ESG is weaponizing the cost of capital and that is leading to under-investment in the fuels we need to get us TO the future. Renewables only work when the sun shines or the wind blows, and we have no efficient manner to store that energy for those times when those requirements cannot be met. The result is fossil fuel shortages and higher energy bills around the globe, and unfortunately, just as winter approaches in the Northern Hemisphere.

- A quick read of the Wall Street Journal this week will see stories about power problems in China, India, the U.K. and to a lesser extent, the U.S. But make no mistake, heating our homes this winter will likely cost materially more than last year.

- The economic consequences are potentially enormous. Shortages, no matter the reason, cause prices to rise. That is a lesson form Economics 101. The result is a decline of the purchasing power of our currency, which puts upward pressure on wages and threatens an inflationary spiral. That pushes us toward the leading edge of an old-fashioned recession. We don’t mean a terrifying crash like 2008 or 2020, but a just a good old fashioned, ‘we’ve gone too far, time to pull back’ recession. However, a recession might be just the thing to fix our current ills. A recession dampens demand, providing supply chains some leeway to catch up. It also reduces the energy requirements of industry, easing the energy shortage too. A recession certainly would not be pleasant, but it may be necessary. Too much Central Bank intervention for too long has made our economy increasingly fragile.

- The bond market appears to be in agreement as the 30-year Treasury auction this week was not only good, it was off-the-charts good. Who would have thought demand for 30-year bonds with very low rates would be so attractive in an environment with sharply higher inflation? The only reason that might be true is that the bond market expects rates to decline, not rise, and that implies weaker economic growth at best and a recession at worst.

What Do Consumers See That Economists Do Not?

- The idea that trouble may lie ahead is certainly not a mainstream idea in the economics community, but the consumer appears to be taking notice of what is happening in the world.

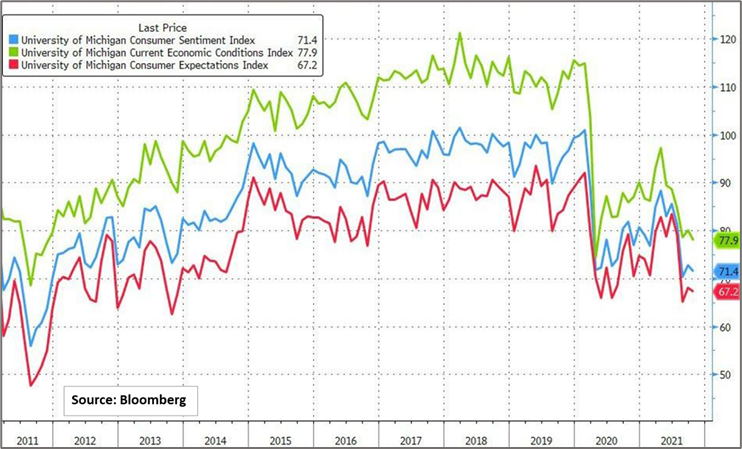

- The latest University of Michigan Consumer survey below shows that Consumer Sentiment (blue line), the Economic Conditions Index (green line) as well as the Consumer Expectations Index (red line) are all at or near the pandemic lows of 2020 and at levels last seen back in the 2011-2013 time frame. Household consumption is more than 2/3 of GDP, so this is not exactly a ringing endorsement of the current economic situation.

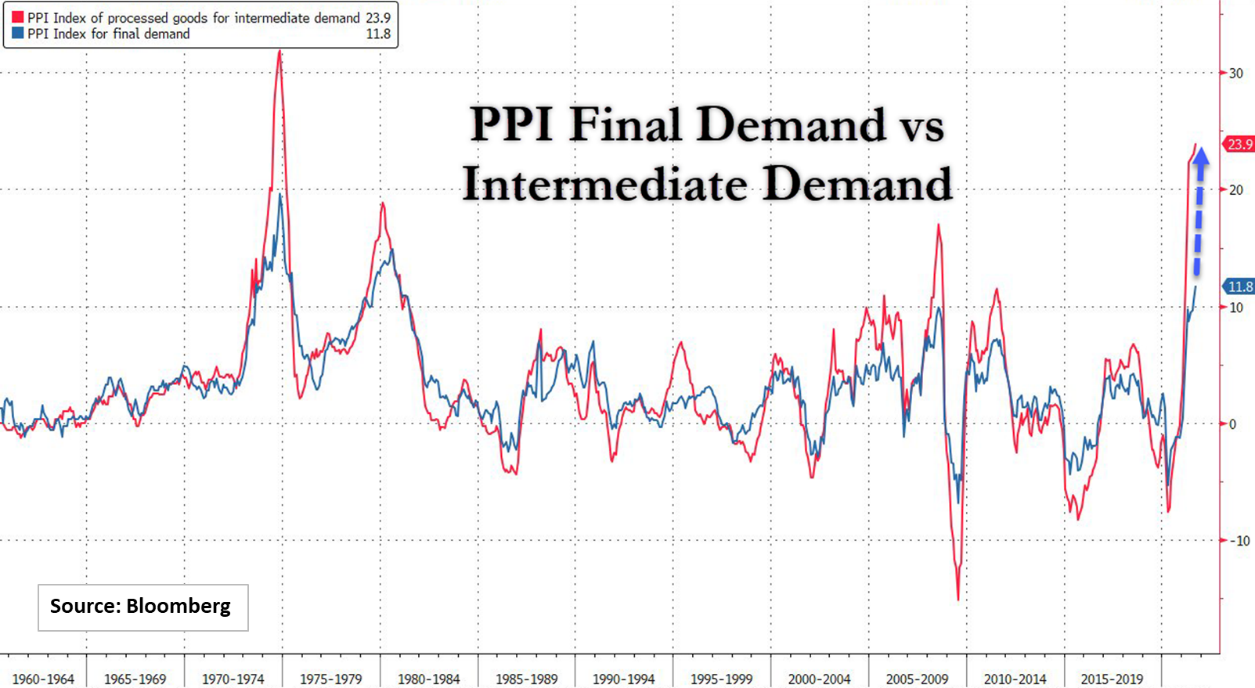

- The Producer Price Index, a measure of inflation for finished goods at the manufacturing level (blue line, following page), ticked up again, albeit slightly less than expected. Somewhat more disturbing is that the PPI index for intermediate goods, i.e., components needed to make finished goods (red line), rose to its highest level since the mid-1970’s. Both of these would imply that inflation at the consumer level is poised to worsen from here.

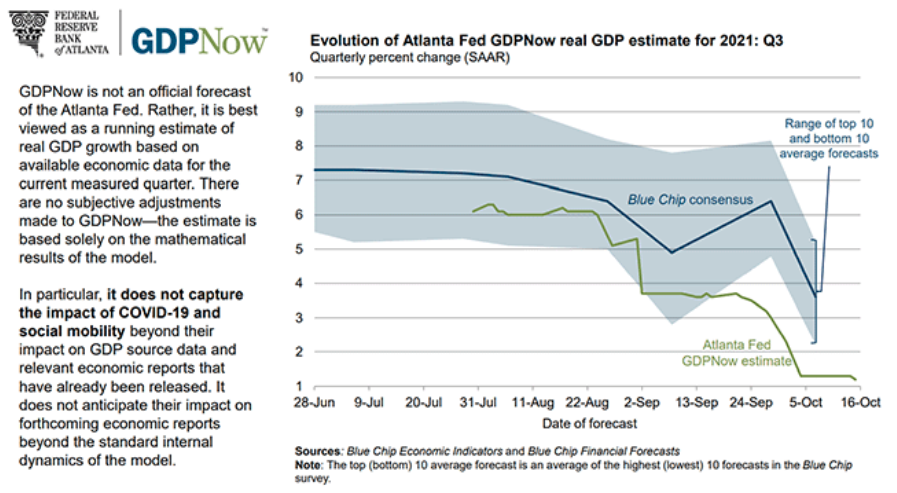

- The Atlanta Fed’s GDPNow model estimate for third quarter GDP ticked down again on Friday to 1.2%. The Blue Chip Consensus estimate for the third quarter GDP has also been falling, but the last reading was still almost 4%. Many economists are forecasting a growth revival in the fourth quarter based on better control of the Delta variant. From our perspective, the most recent data suggests otherwise. If there is going to be a positive reaction to the decline of the Delta variant, it is yet to appear.

What We’re Reading

Reshoring Concerns Are ‘Overblown,’ Vinals Says: IIF Update

British Charger Action Suggests Nervousness About European Switch To EVs

China coal prices hit record high as floods add to supply constraints

Why steel demand is creating a bubble (11 minute video)

The Labor Shortage Is Here to Stay. Businesses Are Adjusting.

From Construction to Hollywood: Unions demand higher pay, better hours

Biden Confronts Supply Chain Crisis Stretching Past His Grip

Consumer prices rise more than expected as energy costs surge

Ford to suspend production on Friday at Mexico plant on materials shortage

A buried building near Jerusalem’s Western Wall is opening to travelers

Retirement Planning:

Spend The Right Money First When You Retire

In what order should you spend the money you have saved for retirement?

Tax Planning:

KPMG 2022 personal tax planning guide

Health:

Wheat Bread Isn’t Actually The Best For Weight Loss, Says New Study

Research shows there’s a completely different loaf you need to buy.

Entrepreneur:

Three Signs You’re an Entrepreneur at Heart

How do you know that you have what it takes to become an entrepreneur?

Disclosures:

Palumbo Wealth Management (PWM) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where PWM and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at www.palumbowm.com

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter, will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Consumer, Energy, Federal Reserve, GDP, Inflation, Microeconomics, Money, Price Inflation, Recession Concern, Shortages, Weekly CommentaryArticles, General News, Weekly Commentary

By: Adam