Supply Shock

If you think this is another story about oil, you are mistaken. The law of supply and demand works throughout any free economy. It states that less supply should result in higher prices, other factors being equal. This is certainly true for oil, as we have recently experienced, but the same dynamic applies to the stock market.

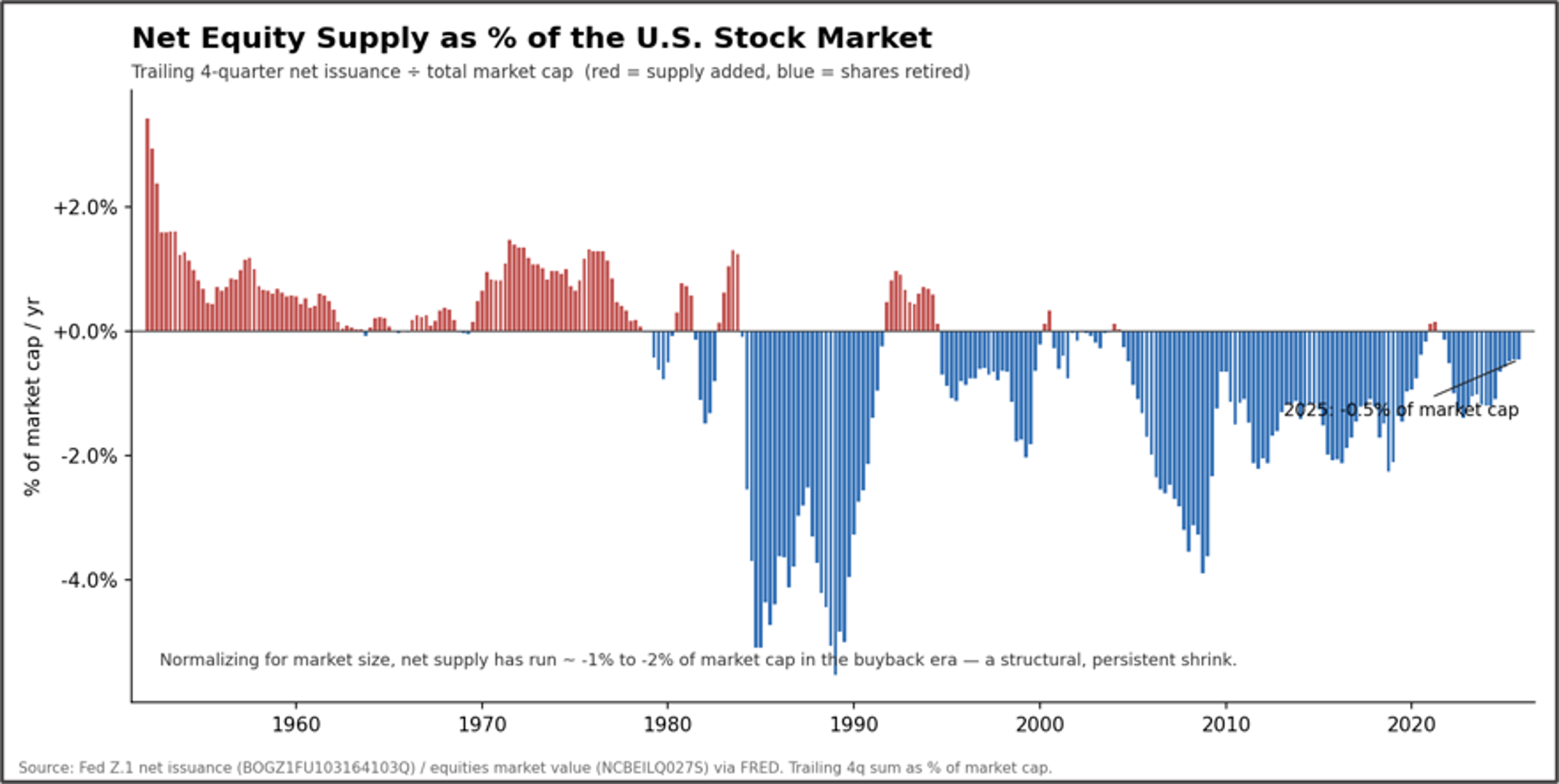

Equity returns are higher when the supply of stocks is shrinking. Conversely, returns are more subdued when supply is rising. It now appears that the supply of stocks, which has been shrinking with remarkable consistency since the early 1980’s, is about to flip and begin growing. The string of recent record-high index levels might trick you into believing that supply has also been increasing, but that is not the case.

Net equity supply is calculated by taking new share issuances, such as IPOs and secondary offerings, and subtracting stock buybacks and corporate acquisitions. Rising stock prices do not increase the supply of shares. Prior to 1982, net equity supply was consistently rising because corporate buybacks were legally restricted and viewed as stock manipulation. That dynamic flipped in 1982 when new regulatory rules permitted companies to buy back their own shares under defined guidelines.

Since that policy shift, corporate share buybacks totaling trillions of dollars have caused public equity supply to shrink. Normally, this shrinkage might be offset by IPOs and secondary offerings (shares sold by companies that are already public). However, that has generally not been the case. The surge in available private capital over the last several decades has allowed companies to remain private much longer. Combined with the much heavier regulatory burdens of the public markets, companies have been willing to delay IPOs and, as a result, limit new supply.

When you put these items together, you get a long period of declining equity supply, shown in the blue bars below. When net equity supply is positive, the growing availability of shares requires a continuous influx of new investor capital just to sustain current prices. Conversely, when net equity supply is negative—meaning corporate buybacks outpace new listings—the public equity pool shrinks. This creates a scarcity value that naturally supports higher stock prices.

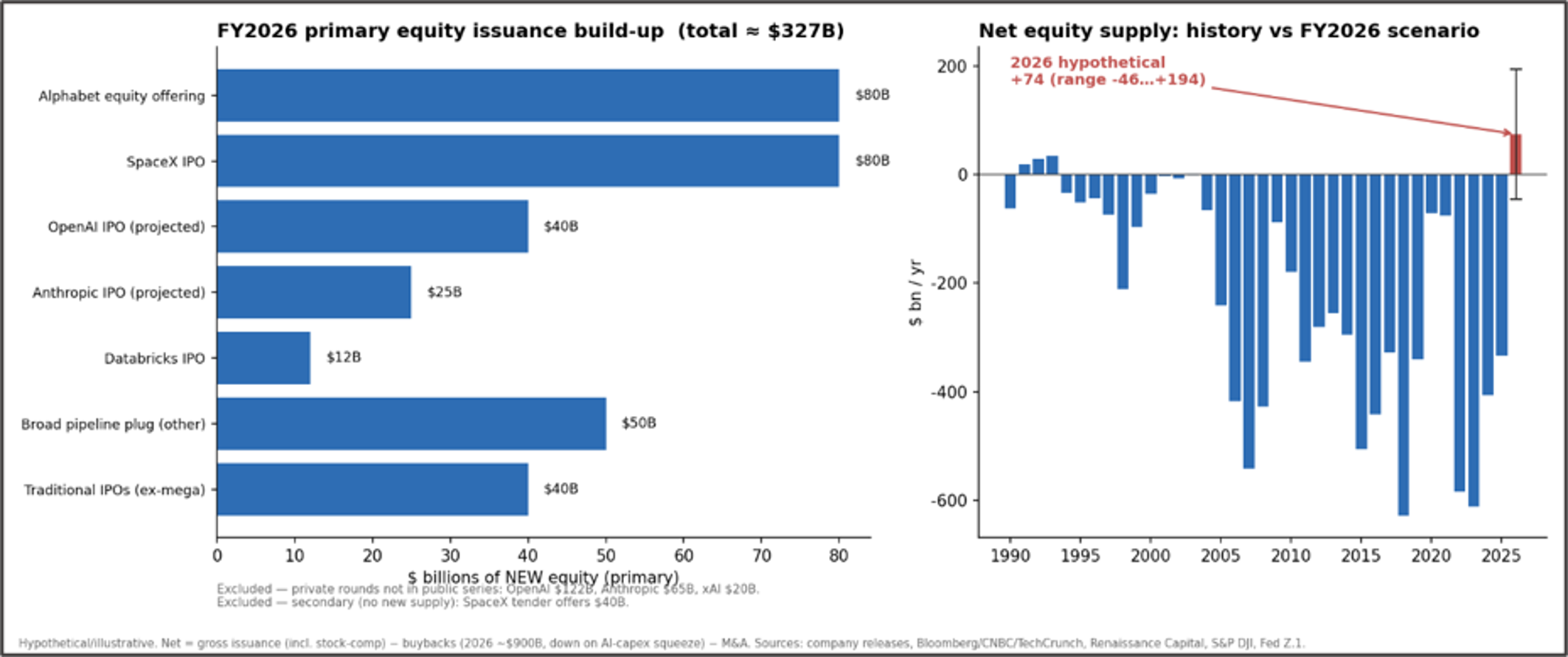

This multi-decade trend of reduced share supply now appears to be reversing. A combination of major new tech IPOs entering the market and a substantial reduction in buyback activity from tech “hyperscalers”—who are redirecting their massive cash reserves into building data centers—is flipping the scale. This year, there looks to be a projected increase in equity supply of roughly $74 billion. Of course, this completely depends on these very large IPOs coming to market and continued investment in data centers as opposed to share buybacks.

Just this week, Alphabet (GOOG/GOOGL) announced equity offerings totaling $80 billion and Meta shares declined ~6% on Friday on rumors that they are also set to sell ‘tens of billions’ in new stock, reversi9ng many years of net stock repurchases. If tech remains the stock market focus, there are plenty of private companies that will be looking to go public in the coming years, adding to supply. It is estimated that there are about 1,200 venture-capital-backed, so-called “unicorns” (private companies with valuations of $1 billion or more). In short, the supply of new equity is building on the sidelines.

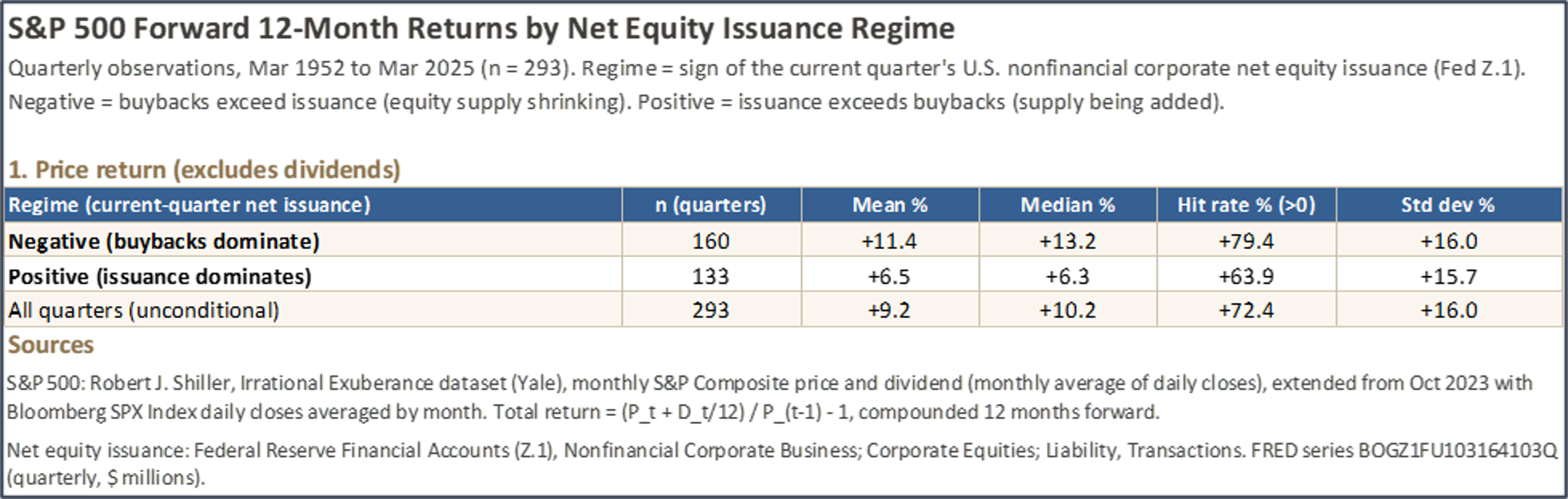

Historical data confirms that these shifts in equity supply could matter immensely to investors. When equity supply is negative and corporate buybacks dominate the market, average stock returns twelve months out are roughly twice as high as the returns achieved when equity supply is positive. With the stock market at new highs and equity supply likely to turn positive in the coming months, it could be time to reduce stock return expectations after the recent run up in the S&P 500.

The evidence is in the table above, which examines quarterly data from 1952 through March 2025. When in a negative supply regime (where buybacks dominate), the median index return was 13.2%, and 79.4% of the 293 quarters examined had a return greater than zero. When in a positive supply regime, the median index return was only 6.3%, and only 63.9% of the quarters had a return greater than zero. We also note that despite the substantially lower returns, the volatility (standard deviation) of the returns was quite similar. The positive supply regime had little influence on risk.

Late this week, the AI mania lost a bit of luster. Will that influence the pricing or timing of the pending mega-IPOs? Time will tell, but we have to recognize the potential for a short-to-intermediate-term “oversupply of equities” hitting the markets if these IPOs are successfully brought to market. While it is not necessarily a bad thing long-term, in the short term it has the potential to depress the equity markets and create more volatility as funds adjust portfolios for the SpaceX IPO and others to follow.

SpaceX Update

Last week, we wrote about the potential influence of mega-IPOs on indexes. We noted that NASDAQ had already altered the requirements for inclusion in its indexes. This week, S&P weighed in and took the opposite course. They made no changes to the qualifications for inclusion in the S&P indexes. That means the earliest SpaceX could be included in the S&P 500, and other S&P indexes, would be one year after its IPO. It may not even happen then, as profitability is also a requirement for inclusion, and it might take some time before SpaceX reports profits.

Have a great week!

What We’re Reading

-

Alphabet is seeking fresh capital as stock’s 4-week losing streak tests investor appetite

-

U.S. payrolls rose by 172,000 in May, much more than expected

-

The robot that can outplay elite table tennis players

Palumbo Wealth Management (PWM) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where PWM and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at www.palumbowm.com.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be dependable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

All information has been obtained from sources believed to be dependable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that no such statements are guarantees of any future performance, and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

Past performance is no guarantee of future returns.

Alphabet, equity returns, Google, IPOs, mega IPOs, SpaceXBy: Adam