Retirement Isn’t a Four-Letter Word

Each year J.P. Morgan releases an educational booklet on retirement and because we focus so heavily on retirement for clients, we have made it a practice of taking a few topics from it for our clients.

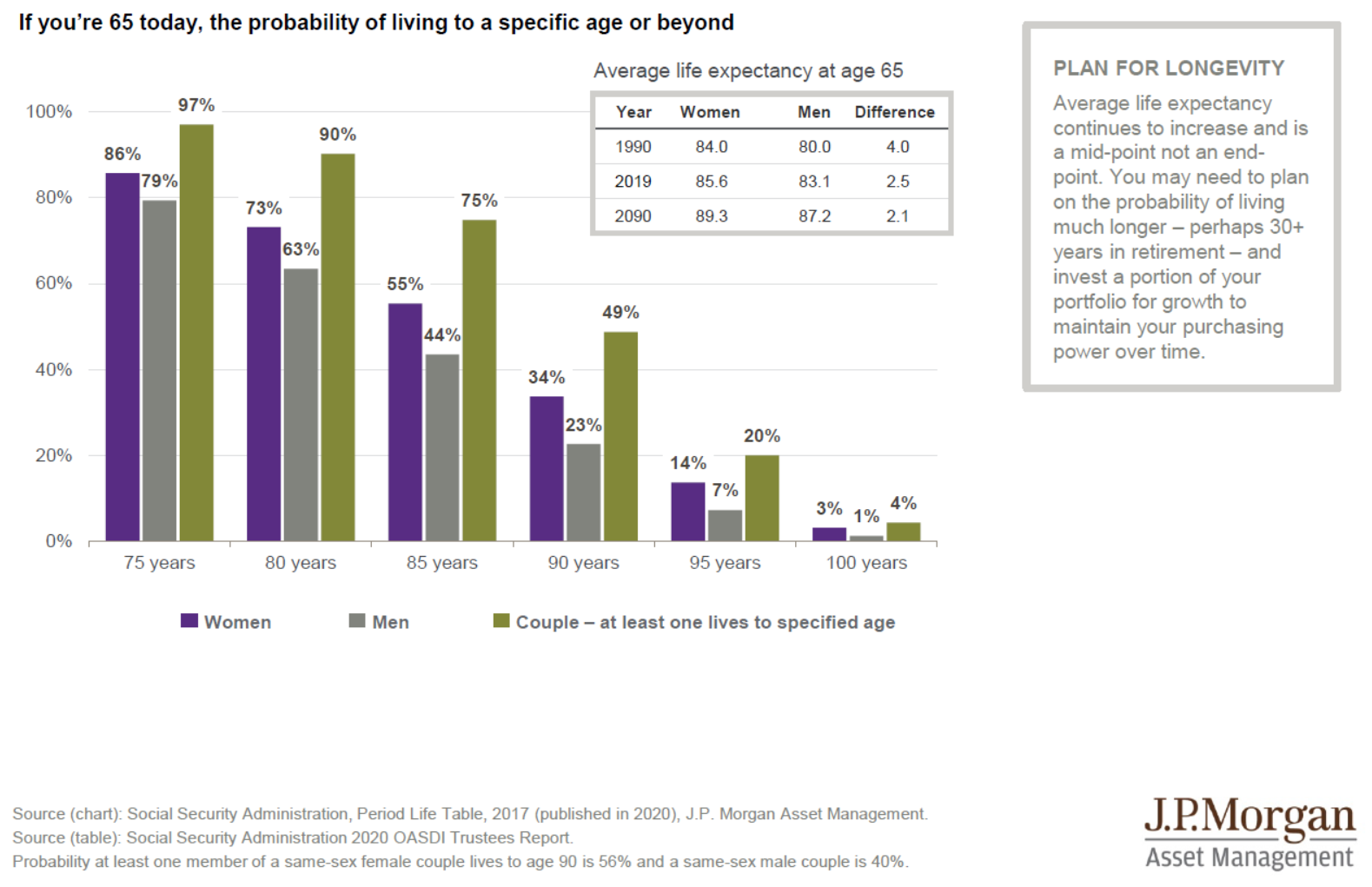

Longevity: The first topic we want to address is longevity. We have always been fascinated by the fact that most people tend to underestimate how long they will live. This affects retirement in a multitude of ways. Our planning process is designed to be as accurate as possible so that you do not run out of money in retirement and your life expectancy is a critical part of that analysis. We typically plan for a 100-year lifetime, which sounds excessive, but despite longevity declining in 2020 due to COVID, life expectancy is likely to get higher over time. Here is what the statistics say:

If you are 65 years old today, the probability of living to 85 or beyond is 55% for a woman and 44% for a man. (See chart at top of next page.) More importantly, for a couple, both age 65, the probability of one living to age 85 is 78%, and the probability of one living to age 90 is 49%. Let that sink in for a moment…. For a couple age 65 today, there is essentially a 1 in 2 chance that one will live to age 90. Extend that out by five years and there is a 1 in 5 chance that one will live to age 95. Planning for long retirements is not an option, it is mandatory.

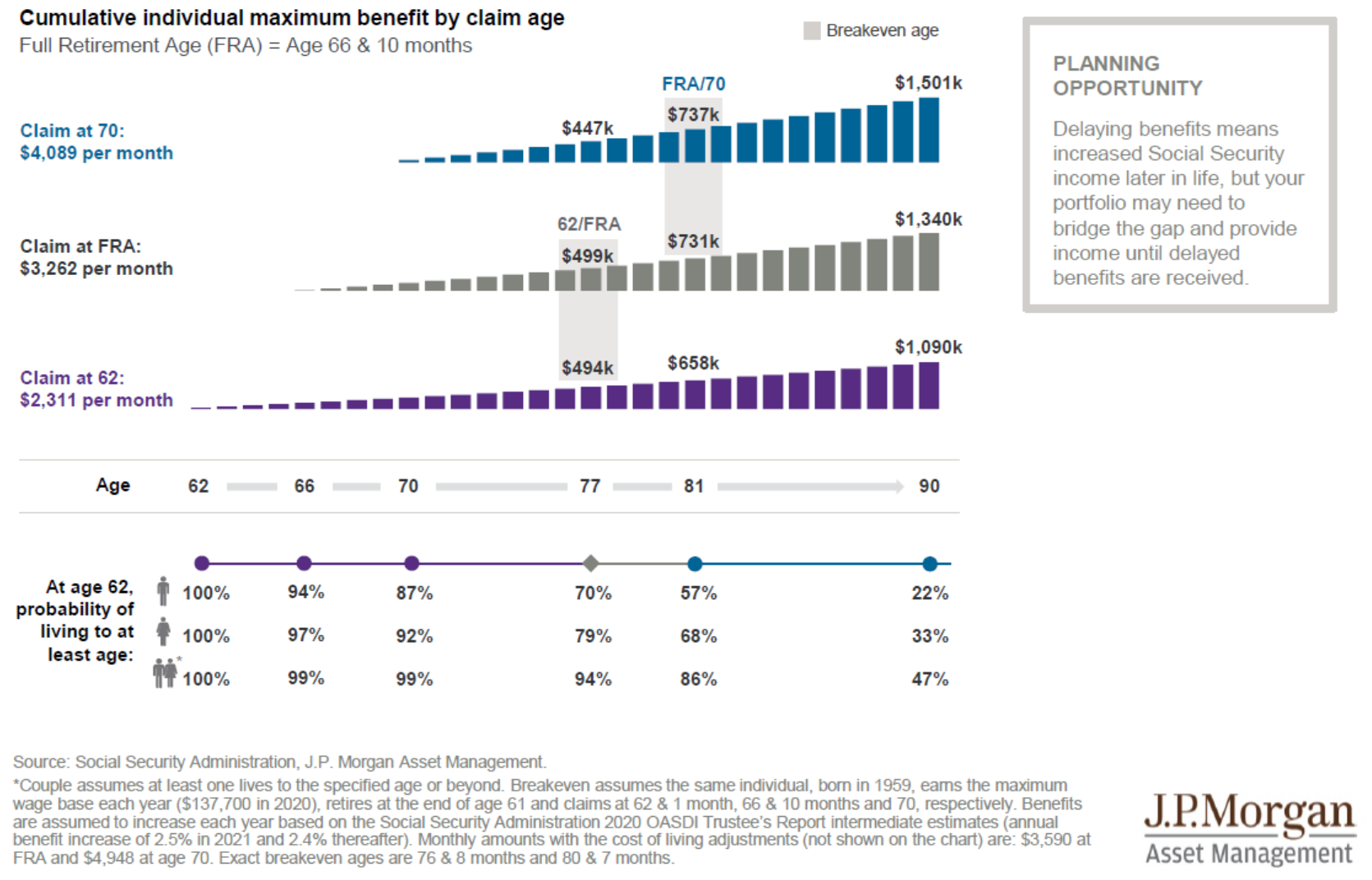

It also makes a difference for Social Security options. It is important that you stop thinking of Social Security as a retirement plan. It isn’t. It is a second-to-die, inflation-adjusted annuity. If you were to purchase such an annuity in the open market today, it would be incredibly expensive and you are getting it ‘for free’ so choosing your Social Security options wisely is important.

The Social Security ‘breakeven’ is about age 81 (see chart at bottom of next page), meaning that if you take your Social Security at age 70, rather than at age 62, you need to live into your early 80’s to ‘get back’ the money you did not take from age 62 to 70. But that is a faulty analysis as it ignores the second-to-die functionality of Social Security. If one spouse dies, the other spouse receives roughly the same amount as the person with the highest benefit. The point is that even if you die, your benefit can continue for your spouse. That complicates the analysis greatly. (We are always available if you would like some advice on your Social Security options.)

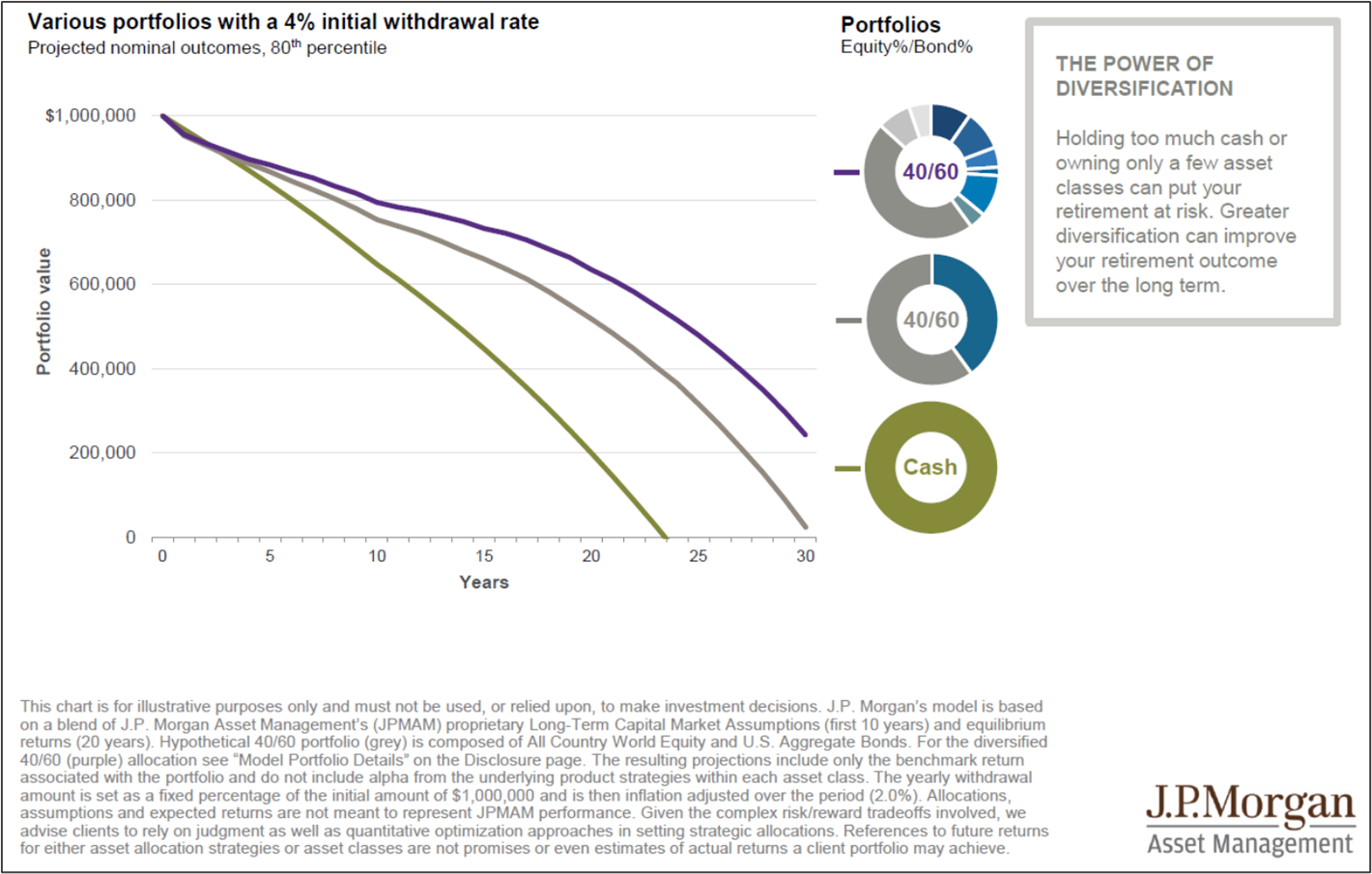

Your Retirement Portfolio: Investing for retirement is also complex because we have no control over market returns. However, we do have some control over how that portfolio is invested. Our risk-balanced approach to investing produces a diversified portfolio that has historically performed well over time, which comes with the standard caveat that past results do not assure future results. But diversification in a portfolio allows investors to do several important things:

- It Allows Investors to Stay Invested. There is always the temptation to try to time the markets. Tough times makes us want to sell and run for the hills, attempting to avoid the disaster du jour. In our view, timing the market consistently is impossible. Here’s why: in 2020, seven of the best 10 days occurred within two weeks of the 10 worst days. Six of the seven best days occurred after the worst days. The second worst day of 2020 – March 12 –was immediately followed by the second-best day of the year. That’s why it is so important to stay invested and stay diversified.

- It Can Improve Returns Over Time. The chart on the next page shows two hypothetical J.P. Morgan portfolios and cash, using a 4% withdrawal rate for the portfolio. The 40/60 portfolio lasts approximately 30 years in the example while the more diversified 40/60 portfolio still had roughly $200,000 remaining after 30 years.

These are hypothetical returns using indexes and do not assure any future return, but historically, more broadly diversified portfolios offer the opportunity to improve risk-adjusted returns over time when compared with similar, but less diversified portfolios. Improved returns would then lead to more assets available during retirement. The lessons from J.P. Morgan are clear: the path to a productive retirement lies in a solid investment framework and a well thought out plan and that’s why we are here for you and your family.

In spite of the cost of living, it’s still popular.

The title is attributed to Kathleen Norris, poet and essayist, and we might add humorist. But inflation is unfortunately, not a laughing matter. Inflation has been a hot topic of late and even more so as the latest COVID relief bill was signed into law. We thought it would be useful to explore the two key inflation measurements, how they are similar and different, and how Fed inflation policy might impact our lives in everyday terms.

The Key takeaways are:

- The Fed’s preferred inflation measure is PCE (Personal Consumption Expenditures), not the more common CPI (Consumer Price Index).

- CPI inflation tends to run higher than PCE inflation, on average.

- The Fed’s desire for 2% inflation is based on PCE, which implies that the Fed wants CPI to run even higher than 2%.

- The Fed has expressed a willingness to allow inflation to ‘run hot’ for a period of time thus bringing the long-term average inflation up to the 2% target. Again, this implies that CPI would be allowed to run even higher before the Fed becomes concerned.

- The stage is set such that inflation could become a more serious problem if the Fed loses control.

Two Inflation Measures – PCE and CPI

There are two primary ways inflation is measured. The first is the Consumer Price Index (CPI) which garners most of the headlines and is used for adjusting inflation protected bonds as well as social security benefits. The other, lesser-known inflation measure is the Personal Consumption Expenditure Index (PCE). The PCE is important because it is the tool the Fed uses to measure inflation.

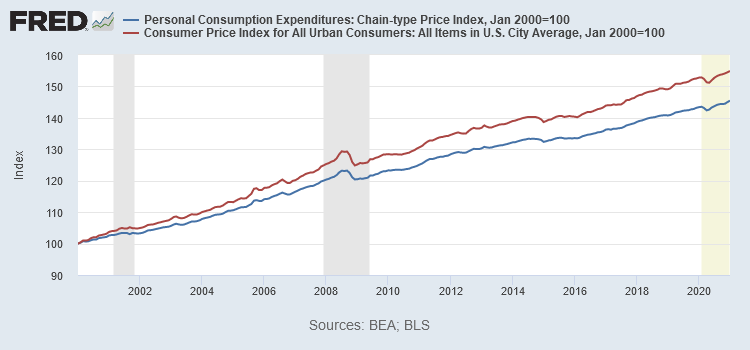

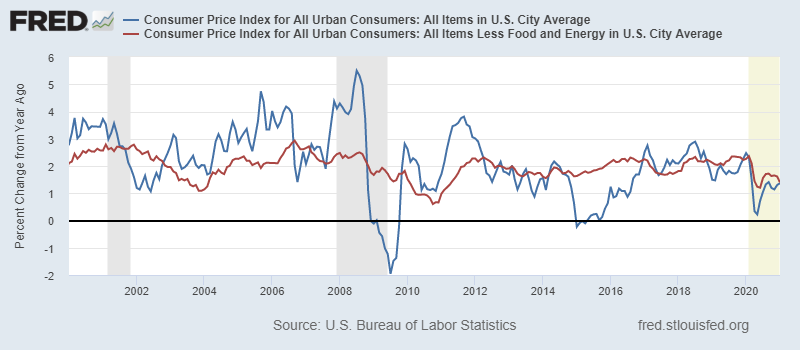

These two inflation measures follow similar trends but are far from identical. As shown at right, the CPI tends to systematically report higher inflation than PCE. Since 2000, prices, as measured by the CPI, have risen by 54.9%, while those measured by the PCE have risen by 45.5%. This implies that on average, CPI inflation has run about 0.3% higher than PCE inflation since 2000.

If both of these are designed to measure inflation by using a basket of goods, why the difference? There are three factors that create the difference – the weight effect, the coverage effect and the formula effect.

- The Weight Effect – People spend more on some items than others, which implies the weight of that item is heavier than other items. As an example, most people spend more on gasoline than they do on bread, so the gasoline will have a heavier weight in the calculation. Most of the difference between CPI and PCE are explained by different weights in the baskets of goods. The CPI basket is what households are buying and the PCE basket is based on what businesses are selling

- The Coverage Effect – CPI only measures out of pocket expenses for goods and services. It specifically excludes items that are paid for by employers or insurance companies, for example. PCE includes these items.

- The Formula Effect – CPI is a relatively fixed basket of goods. PCE, on the other hand, attempts to account for substitutions which might occur as prices change. As an example, if the price of eggs rises substantially, the PCE might adjust by assuming more breakfast substitutes, like cereal, in the basket, and fewer eggs.

Core vs. Headline Inflation

Both the CPI and PCE inflation measures come in two basic flavors – Headline Inflation and Core Inflation. In both cases, headline inflation includes the entire basket of goods while core inflation excludes food and energy in the calculation. Food and Energy make up a large part of the basket for the average American, but these are excluded in the core calculation because food and energy prices are so volatile. That volatility is obvious in the blue line in the chart above. The critical element is that the food and energy portion keep coming back to the average for all other goods.

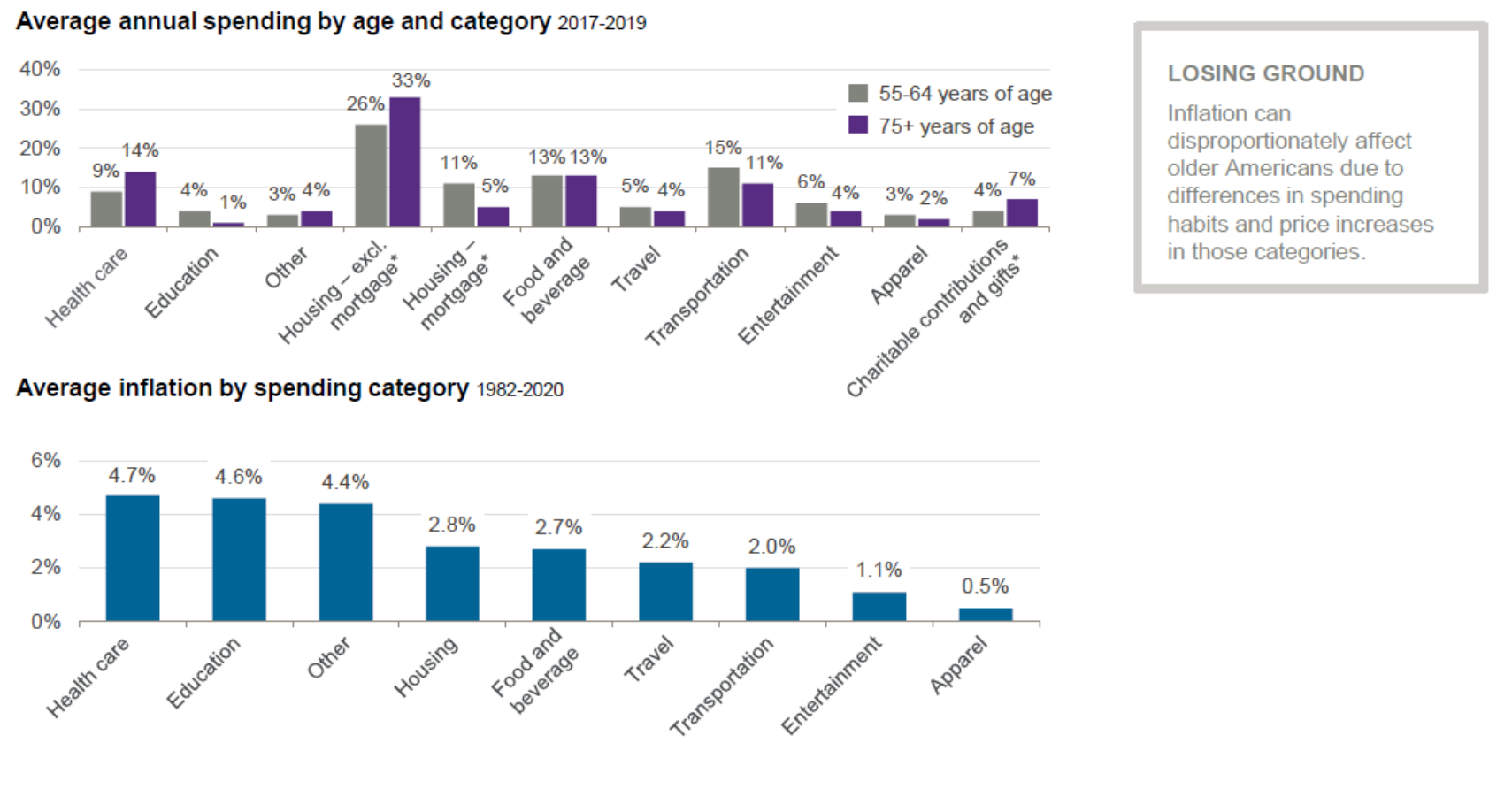

The question of whether CPI or PCE are accurate in measuring inflation is the subject of much debate. We won’t get into that here, but a look at the chart below makes it clear that the inflation we experience can be very different based on how we spend our money. The cost of health care in retirement is a substantial and growing expense and one which has been experiencing a much faster inflation rate. The inflation rate we actually experience can be quite different than the official statistics.

What We’re Reading

Asset bubbles and where to find them

Biden’s American Rescue Plan: Here’s What’s In It And What Isn’t

Facebook and Twitter algorithms incentivize ‘people to get enraged’

S&P 500, Nasdaq weighed down by spike in bond yields

10-Year Yield Could Rise Another 50, 75 Basis Points: DoubleLine (5 Min Video)

U.S. consumer sentiment rises in mid-March to highest in a year

Novavax Covid vaccine data looks promising

Big Market Delusion: Electric Vehicles

Record Drought Strains the Southwest

Will Pent-Up Demand Really Supercharge the Economy? Uh-uh, Economist Warns

Retirement Planning:

Get a health savings account now, you’ll thank yourself in retirement

An HSA will help you save for expenses now and in retirement.

Tax Planning:

Three ways to get a bigger stimulus check using your tax return

Here are a few ways you can make sure you get the most money possible.

Estate Planning:

13 Life-Changing Events Your Financial Advisor Can Help Guide You Through

Any time you’re facing a life-changing event or decision, there are likely to be both short-term and long-term financial implications.

Health:

What the New CDC Guidelines Mean for Fully Vaccinated People and Others

The CDC released new guidelines for people who are fully vaccinated against COVID-19.

Entrepreneur:

6 Ways Managers Can Make Remote Meetings More Equitable

Some people may not feel heard in your meetings, but there are ways you can improve engagement.

Disclosures:

Palumbo Wealth Management (PWM) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where PWM and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at www.palumbowm.com

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter, will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Core Inflation, COVID Relief, CPI, Demographics, Federal Reserve, Headline Inflation, Inflation, Investment Return, JP Morgan, Life Expectancy, Longevity, PCE, Portfolio Diversification, Retirement, Retirement Investing, Social Security, Spending, The Coverage Effect, The Formula Effect, The Weight Effect, WithdrawalsArticles, General News, Weekly Commentary

By: Adam