Is Housing About to Become More Affordable?

One of the things we discuss with regularity is the housing market. The rise in real estate prices appears inexorable, but at some point, the basic laws of economics – supply and demand – eventually hold sway. Home prices rising at a much faster rate than incomes reduces demand over time. You can’t buy a house if you can’t afford it. Eventually a tipping point is reached and either incomes have to rise to match the rise in home prices, or home prices need to come down into a better balance with the level of income. The big questions are how and when this correction happens.

This week, we came across a particularly interesting comment by Nick Gerli, CEO and founder of the real estate analytics firm Reventure Consulting, regarding demographics and the housing market. Some further research led us to other comments from Gerli about the housing market today which led us to highlight his work this week.

Gerli makes two key points:

- He believes that we are approaching a major demographic turning point that will not only redefine housing demand but also redefine the size of the homes people desire.

- Although housing prices are still increasing on a national level, prices are actually declining in about half the U.S., and he looks for prices to decline more.

Demography is Destiny

Demography is destiny is a quote attributed to French philosopher Auguste Comte, which suggests that the composition of a population determines its future. This makes some intuitive sense. For example, the aging of the population will lead to growth in demand for healthcare.

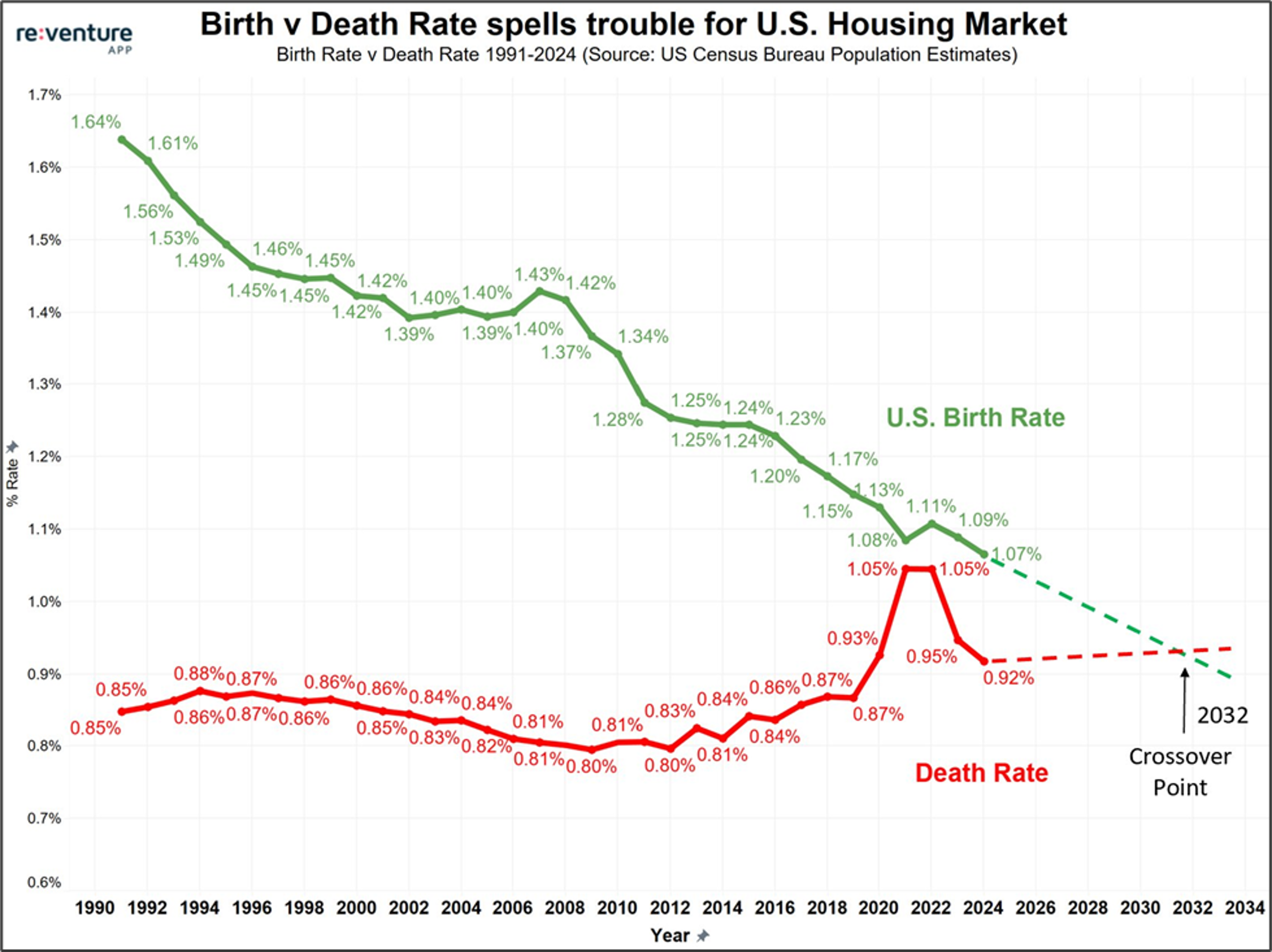

Gerli estimates that by 2032, the number of U.S. deaths will exceed the number of births for the first time, as shown in the chart below. The decline in the birth rate is the continuation of a very long term trend. The death rate, which was declining slightly for many years, began to rise slightly around 2010. Gerli extends that trend, excluding the COVID spike. Making weight loss drugs less expensive might nudge the death rate back down a little, but a crossover certainly appears inevitable.

Why does this matter? Gerli makes two points here:

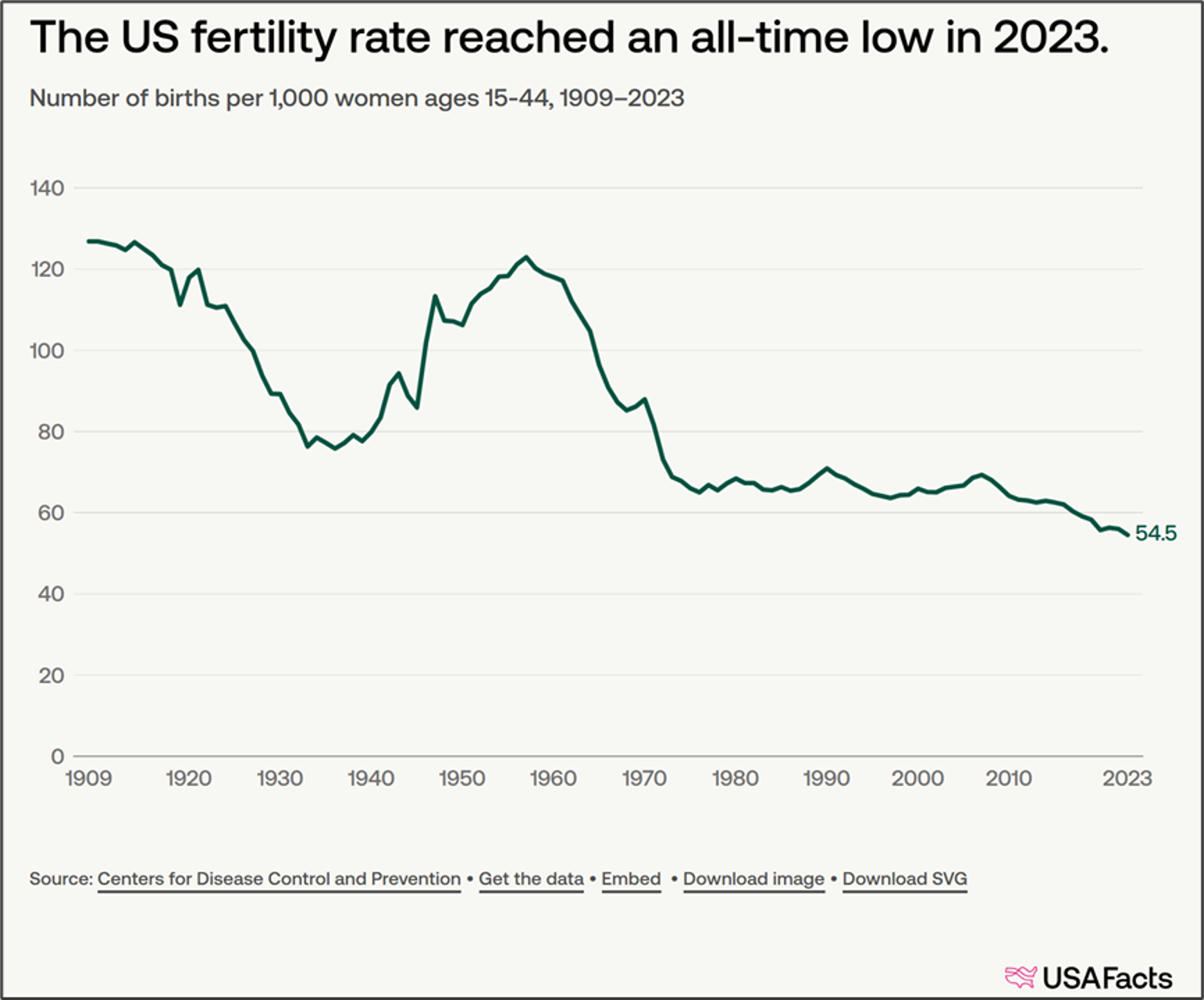

- Demand is Structurally Declining. Declining births implies declining family formation, therefore reducing the aggregate need/desire for young people to buy houses. Declining birth rates are also a function of the aging of the U.S. population. As the median age increases, there are fewer people of the age who would have a child as a % of the population. Finally, the fertility rate among women aged 15-44 has dropped significantly in the last 20 years. Whether this is simply a societal shift or a reaction to the high cost of child care, the result is the same – a declining birth rate. Fewer children will invariably lead to lower homebuyer demand. In addition, demand for 4/5 bedroom houses should also decline if family size declines.

- Supply is Structurally Increasing. The number of deaths increases as Baby Boomers age out, thereby increasing available housing inventory. Freddie Mac estimates new supply from this source at 9 million homes (cumulatively) by 2035.

Both of these factors are likely to have a disinflationary, or even deflationary impact, on home prices over the long-term and it is a trend that is already firmly in place. Although these changes are undeniably occurring, the change arrives gradually. Exactly when the housing market reaches a tipping point due to these factors is hard to predict and in reality, it will arrive at very different times in different locations.

What’s Happening Today?

The demographics will dictate the long term, but the housing market remains in an almost locked state as those with low-rate mortgages are largely unwilling to give up that advantage. However, Gerli believes that we are entering a ‘disinflationary/deflationary vortex’ and that the US is on the precipice of a big decline in home prices that can continue into 2026.

What Are the Signs?

- Weak Buyer Demand: Affordability is a constant source of political debate. The problem is that the current mortgage debt payments represent 38% of income, according to the ICE Mortgage Monitor. That is historically very high and is clearly dampening demand.

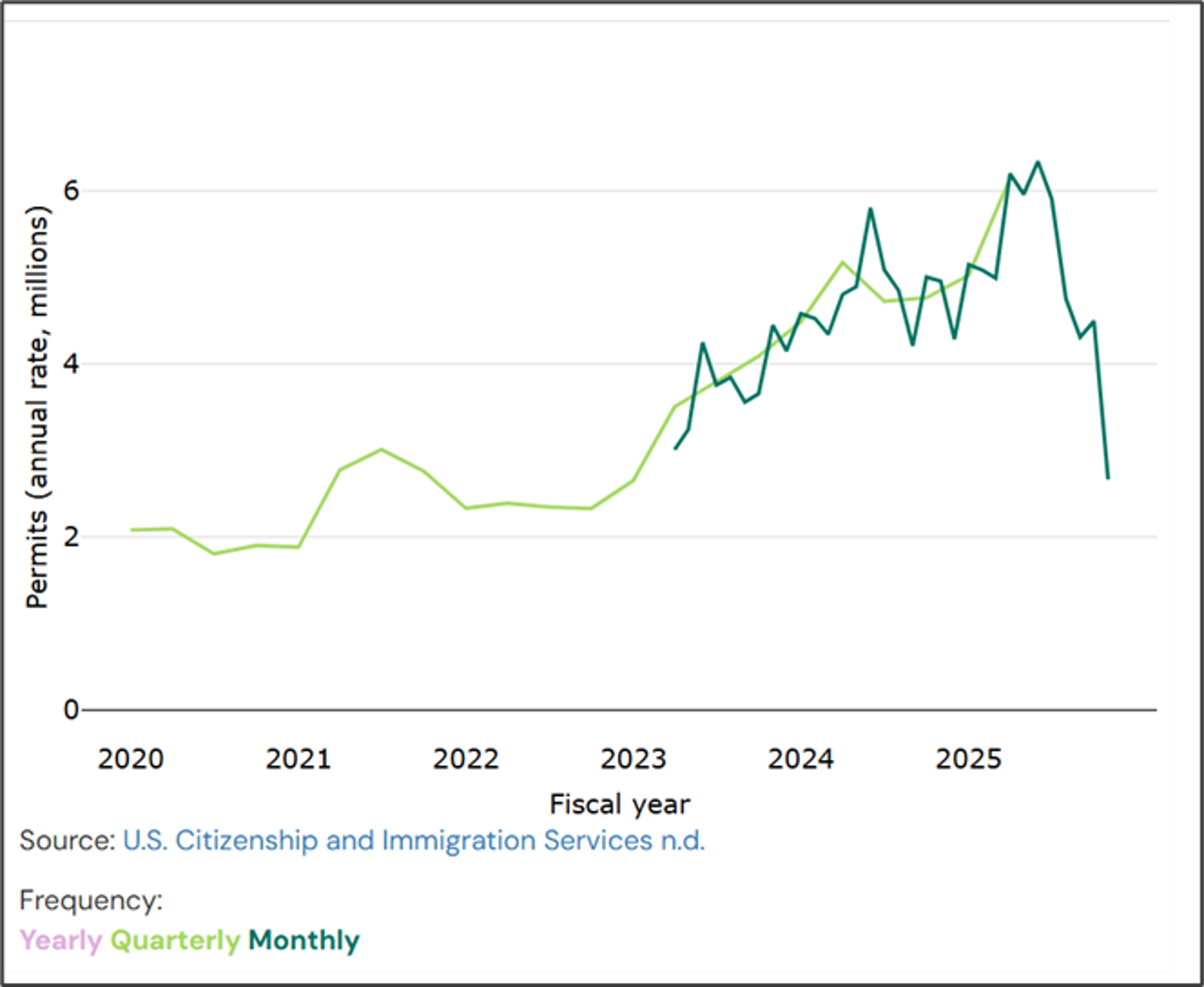

- Weakening Rental Demand: Rental affordability is less of an issue, but rents are facing several headwinds, including lower population growth/immigration growth and recently some hiring weakness. Work permit applications (shown below) have plummeted, which does not bode well for rental demand and rent growth is the slowest it’s been in 14 years, according to Gerli.

- New Supply entering the market: There was a big pipeline of new construction over the past 3-4 years that is now adding to supply, just as demand is weakening.

- Investor-owned properties: Weakening markets will likely draw additional supply as investor owned properties (about 25% nationwide) come under some stress. (WSJ – Rise of ‘Accidental Landlords’ Is Bad News for Investors Who Bet Big on Rentals)

In summary, Gerli sees weaker rental as well as purchase demand, just as a surge in new supply enters the market. Any further weakness, especially in rental markets, appears likely to push more supply onto the market as investor owned properties look to exit a weak market. All of this has the potential to pressure housing prices lower over the next year to 18 months.

Broader Implications

- Decline in personal Wealth: In many ways, the events Gerli is anticipating are ultimately very good for the economy because it should return housing prices to a more normal relationship with income, making homes significantly more affordable than they have been since the early 2000’s. That is clearly a good thing but getting there would logically entail some pain. Homes are often a significant portion of personal wealth, so declining home values would pinch the wealth expectations of many homeowners.

Room for Interest Rate Reductions: About 40% of the CPI is based on housing. Disinflation or outright deflation in housing would serve to keep a lid on overall inflation as measured by CPI, leaving the Fed room to lower rates without the threat of renewing inflation. Lower rates would be generally supportive of equity prices.

Since the 1990’s internet bubble, the U.S. has been through a series of events that have invited ever increasing government intervention in the economy, often with unintended consequences, such as stubbornly high real estate prices. The ability to finally return markets to a better balance would be most welcome in the long run.

Have a great week!

What We’re Reading

- Why The Risks Of Buy Now, Pay Later May Outweigh The Rewards

- Fleet of UPS planes grounded after deadly crash expected to miss peak delivery season

Palumbo Wealth Management (PWM) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where PWM and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at www.palumbowm.com.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance, and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

Past performance is no guarantee of future returns.

affordability, Demographics, Housing, Housing Market, rental housing

By: Adam